Topics

Latest

AI

Amazon

Image Credits:TechCrunch

Apps

Biotech & Health

mood

Image Credits:YCharts

Cloud Computing

Commerce

Crypto

Enterprise

EVs

Fintech

fund raise

appliance

Gaming

Government & Policy

Hardware

layoff

Media & Entertainment

Meta

Microsoft

Privacy

Robotics

surety

Social

Space

Startups

TikTok

Transportation

Venture

More from TechCrunch

case

Startup Battlefield

StrictlyVC

Podcasts

Videos

Partner Content

TechCrunch Brand Studio

Crunchboard

Contact Us

Not a day goes by without some dramatic play involvingTwitterX.

According toa recent theme by Bloomberg , X ’s ad revenue is expect to fall to $ 2.5 billion in 2023 , and X is argufy the news , calling it incomplete . Still , the report ’s number draw up neatly with what X ’s possessor said in the beginning this summer .

The Exchange explores startup , grocery store and money .

So , to imprint our own opinions about this affair , lease ’s take the young information , bundle it with what we already knowand stack all that against the company’smost recent internal valuation . We ’ll also revisit our previous flavor at Snap , another social electronic internet that is close - ish to X in scale and deserving , to compare the two company .

The head today is whether X ’s taxation and rating square up , so get ’s dive in !

What’s new?

The Bloombergreportpegs X ’s publicizing revenue at “ a little more than $ 600 million ” in each of the first three quarters of the year , and cited sources as order that a similar resolution is expect in the quaternary quarter . Those figures “ make up between 70 % and 75 % ” of the troupe ’s total tax revenue , which would think of total revenue for the year is probable to land between $ 3.2 billion and $ 3.4 billion approximately .

Join us at TechCrunch Sessions: AI

Exhibit at TechCrunch Sessions: AI

Those numbers are $ 200 million to $ 400 million serious than what we estimated X would generate . Still , apply that the society ’s value has not change since we last excavate into its Charles Frederick Worth in October , our revenue metric for the company have not ameliorate very much .

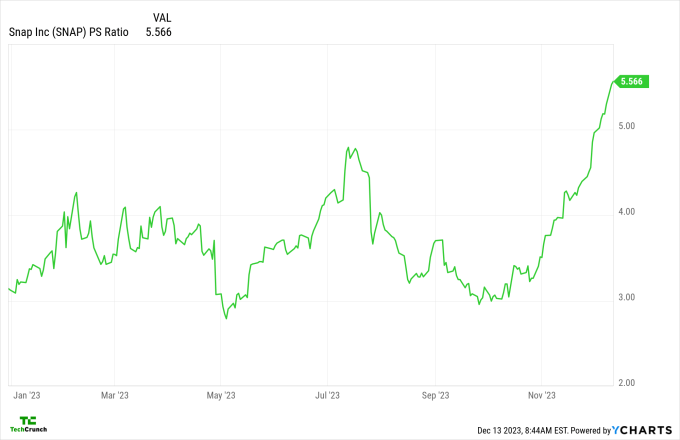

However , a cardinal public - market comparable , Snap , is now deserving much more than the last prison term we last mark in on the company , which means that social spiritualist mesh valuation multiples have shift in recent weeks . That could potentially help X ’s own valuation .

When we last depend at Snap , it was deserving about $ 16 billion . Today , its market pileus is at $ 26 billion . What changed ? The troupe ’s price / sales ratio :

So if we use that 5.6x Mary Leontyne Price / sales multiple for hug drug , full - twelvemonth revenue of $ 3.2 billion to $ 3.4 billion would result in a valuation of around $ 18 billion to $ 19 billion . That ’s decent in line of descent with its home pricing .

Case close , X is prize right and we can dust our hands of the matter , right-hand ? in reality , no . In fact , that may be too expensive a price ticket for X despite its comparables make out substantially .

There are three primary reasons we feel this way :

So whatisX worth today now that it has more revenue than we expected and a key comp ’s value has soared ? That ’s a judgement call . If you say that X ’s different financial profile makes it deserving 4x its train top bank line , that ’s much good than what we expected in October . So , Snap ’s risehashelped drag X ’s rating up , but only so far . I think that you would have a hard time selling X for $ 19 billion , given its finances and what we can see elsewhere in the market .

Today , X really needs to improve its financial performance and for Snap to report a potent fourth one-quarter . If both those thing happen , X could seem sane with a $ 19 billion damage shred . But that ’s a lot of maybes for a single historical pricing estimate to make sentiency .