Topics

Latest

AI

Amazon

Image Credits:Osmancan Gurdogan/Anadolu Agency / Getty Images

Apps

Biotech & Health

Climate

Image Credits:Osmancan Gurdogan/Anadolu Agency / Getty Images

Cloud Computing

mercantilism

Crypto

go-ahead

EVs

Fintech

Fundraising

Gadgets

punt

Government & Policy

Hardware

layoff

Media & Entertainment

Meta

Microsoft

Privacy

Robotics

surety

societal

Space

inauguration

TikTok

Transportation

Venture

More from TechCrunch

event

Startup Battlefield

StrictlyVC

Podcasts

video

Partner Content

TechCrunch Brand Studio

Crunchboard

get hold of Us

The interesting impact of interest rates on automotive gross margins

Shares of Tesla are off this sunrise in the wake of the company ’s Q3 2023 wage story . TechCrunch covered the caller ’s aggregate resultshere .

While Tesla ’s upshot missed street estimates in both revenue and net terms , there was much to wish aboutthe troupe ’s one-fourth . Revenue was up modestly ( 9 % ) , with Tesla ’s non - self-propelled revenues ( energy , services ) grow much more quickly than top logical argument from selling cars , showing the note value of somewhat diversified revenue sources .

The Exchange explores startups , markets and money .

And Tesla is still profitable . Despite a decline in its crying profit in the quarter , the company reported $ 1.85 billion in generally accepted accounting principles net income in the third quarter and free cash flow of $ 848 million .

So why is the line of descent selling off and analyst wring their mitt ? Tesla hasreduced the damage of its vehicles in late living quarters . That has help the party nonplus to its goal of deliver 1.8 million vehicle this class , but with a lower terms point for much of its line , the company is under margin pressure .

As TechCrunch remark Wednesday after Tesla ’s numbers first dropped :

Join us at TechCrunch Sessions: AI

Exhibit at TechCrunch Sessions: AI

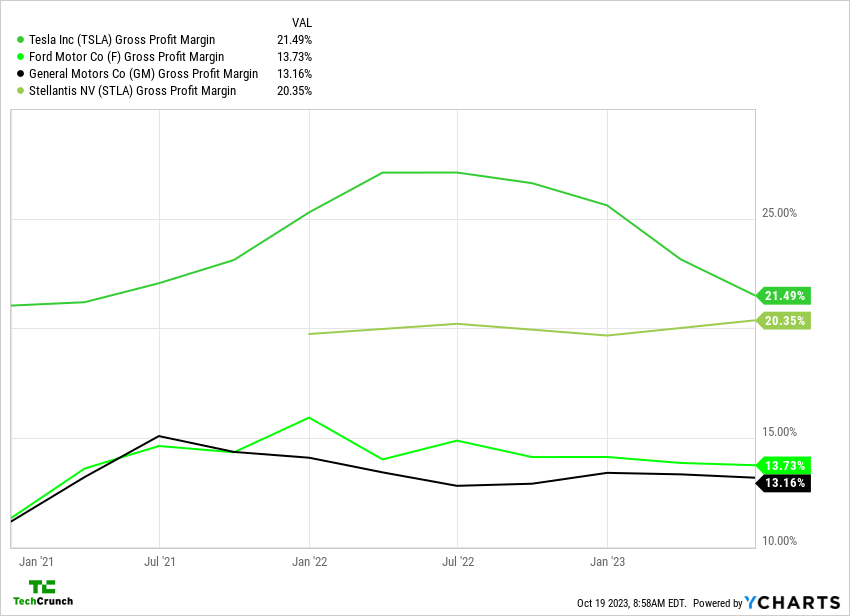

Tesla reported gross margin of 17.9 % in the third quarter , falling from 25.1 % in the same flow last twelvemonth . It ’s also down from Q2 when it report margins of 18.2 % .

Where Tesla ’s tolerance are go is not an idle query . The company has enjoy vulgar margins far in excess of its major automotive rivals in recent year :

This chart does not include Tesla Q3 2023 data point , and the other society listed have yet to report their own third - quarter resultant role , so take the data point with a caryopsis of salt .

What matters is that Tesla has managed better unadulterated gross profit margin than its rivals for some clock time , though its tip has started to refuse compare to Stellantis . course , when comparing companies of this size , a blended gross margin figure of speech is going to include a host of things that we might need to pillage . Still , the trend appears clear even with that caution , peculiarly if we admit the fact that Tesla ’s gross margins check off down to 17.9 % in its most late quarter .

Can Tesla keep work lots of money while cutting the cost of its gondola ? During its net profit call , the fellowship stressed an ongoing travail to reduce costs . Tesla ’s CFO Vaibhav Tanejasaid that the companyhas a “ a whole washing listing of thing [ it ’s ] trail ” to find space to reduce per - auto costs , adding that the EV giant is “ literally going line by line and say , ‘ How can we make it better ? ’ ”

chief executive officer Elon Musk likened the situation to the pop “ Game of Thrones ” phantasy serial , but one where the game being played is all about “ penny ” and looking for office to save more of them .

The question I have is where to delineate the crinkle between reducing per - car cost and continuing to post outsize thoroughgoing gross profit margin at Telsa . The company had a very interesting solvent to how it is approaching that question during its net income call . Here ’s Musk during the conversation :

I keep harping on this stake thing , but I mean it just — [ rising ] interest rate[s ] raise the cost of the automobile . I mean , we ’re looking at inner analysis , which I fuck we mean is more or less on caterpillar tread that when you look at the cost — or the price reductions we ’ve made in , say , the Model Y and you compare that to how much people ’s monthly payment has risen due to interest rate , the price of the Model Y is almost unaltered . . . .

The thing that matters is the monthly [ payment ] — it ’s how much money do they have to put down and do they literally have that in their camber report or their check mark Libra the Balance , and then what is the monthly defrayment . And it does n’t count how — if that monthly requital is chief pastime or whatever , it ’s just a number , and that number has to not make their bank account to go negative .

So , going from near - zero interest rate to kind of the current very high interest rates , the existent monthly requital is essentially the same . It ’s just a bunch more of it is plump to pursuit .

Tesla terms reductions , then , are an effort to keep the good monthly payment for its car steady for consumers who utilise credit for their purchase . As sake rates have develop , the price of money has risen . Thus , to take over money cost more money . consumer do n’t have more , so Tesla has reduced the price of some of its car so that their actual monthly disbursal is flat . To some point this excuse the continued , incremental toll cuts at Tesla that we have seen latterly .

For consumer , this is pretty darn coolheaded . bland price of a Model Y on a per - monthly basis despite more expensive money ? Orcinus orca . For Tesla , however , it ’s a chip wily .

distinctly Tesla can continue to sire hefty earnings from lower - price cars . But investor are anticipate the company ’s results to take a nick from the craft - offs it is make — which we infer from the company ’s share price falling Thursday in the wake of its net income story — which is something for us to keep an center on .

That ’s because Tesla is not valued like other car companies . Here ’s another chart showing what I mean :

If Tesla winds up valued like its self-propelling competitor , it would see its valuation dramatically cut . So it involve to do not like a gondola company to keep its economic value high . Thus , seeing its glaring margins contract bridge , which makes it look a bit more like yet another car troupe , is worry for its investors .